In recent years, Latin America has joined the global Fintech revolution, creating innovative and entrepreneurial ecosystems that enabled the development of new technology startups that offer highly innovative financial products and services. Several studies and reports have highlighted the high growth rates of Fintech in the region, such as the 2017 LAVCA Trend Watch, which pointed out that the Fintech sector represents 25% of the venture investments in IT in the region; or the recently published Fintech Innovation in LATAM report by IDB and Finnovista, where over 700 Fintech startups were identified in Latin America.

Finnovista has conducted different Fintech Radar reports about the most important countries in Latin America in order to create a comprehensive data source of the Fintech enterprises, evaluate the sector’s progress in the region, and give visibility and recognition to a movement that will lead the region towards an ubiquitous and inclusive digital finance landscape. So far, Finnovista has published Fintech Radar studies about Argentina, Brazil, Chile, Colombia, Ecuador and Perú and, on this occasion, Finnovista has conducted an update of the last version of the Fintech Radar Mexico (published in August 2016 by Finnovista).

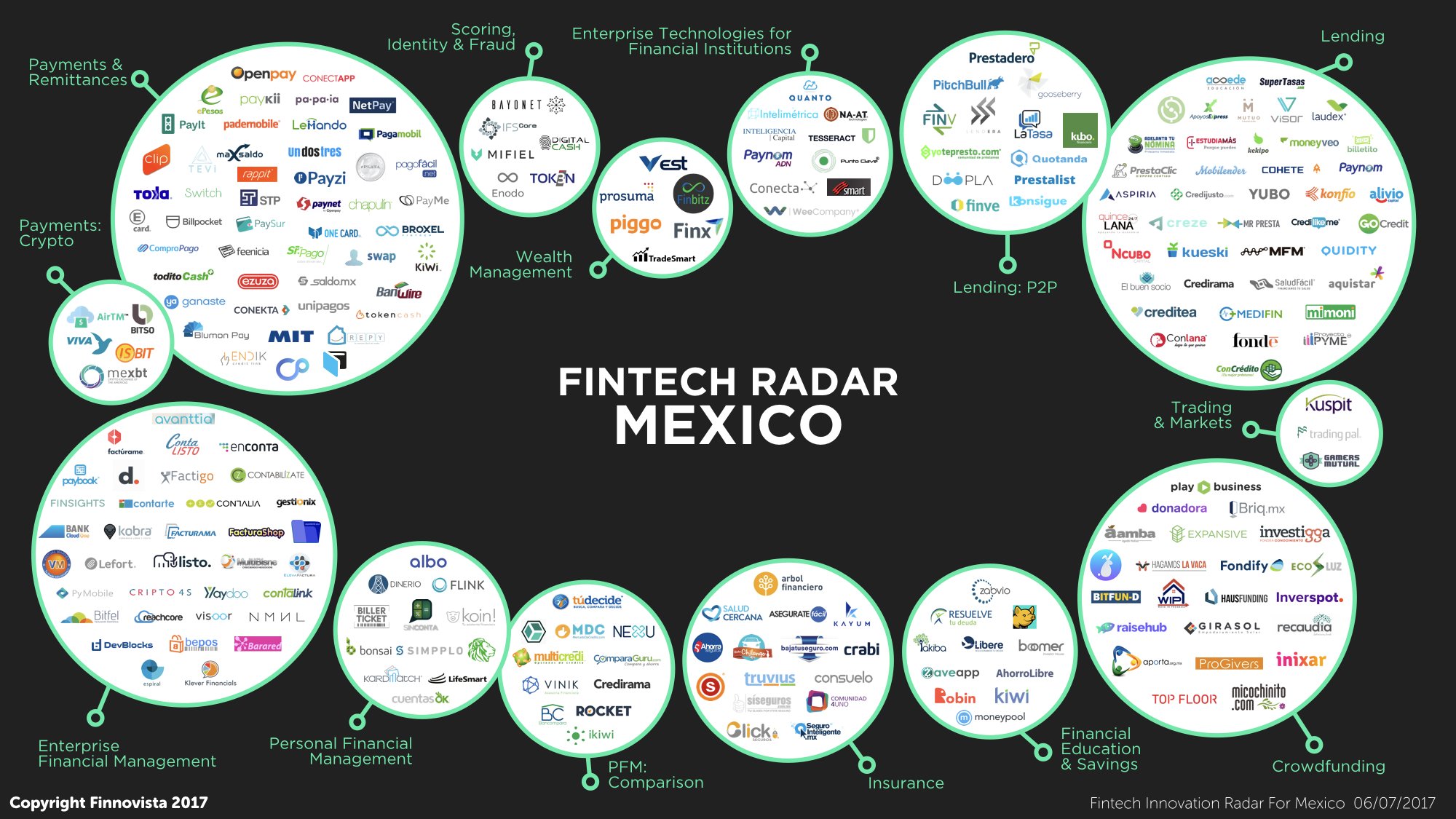

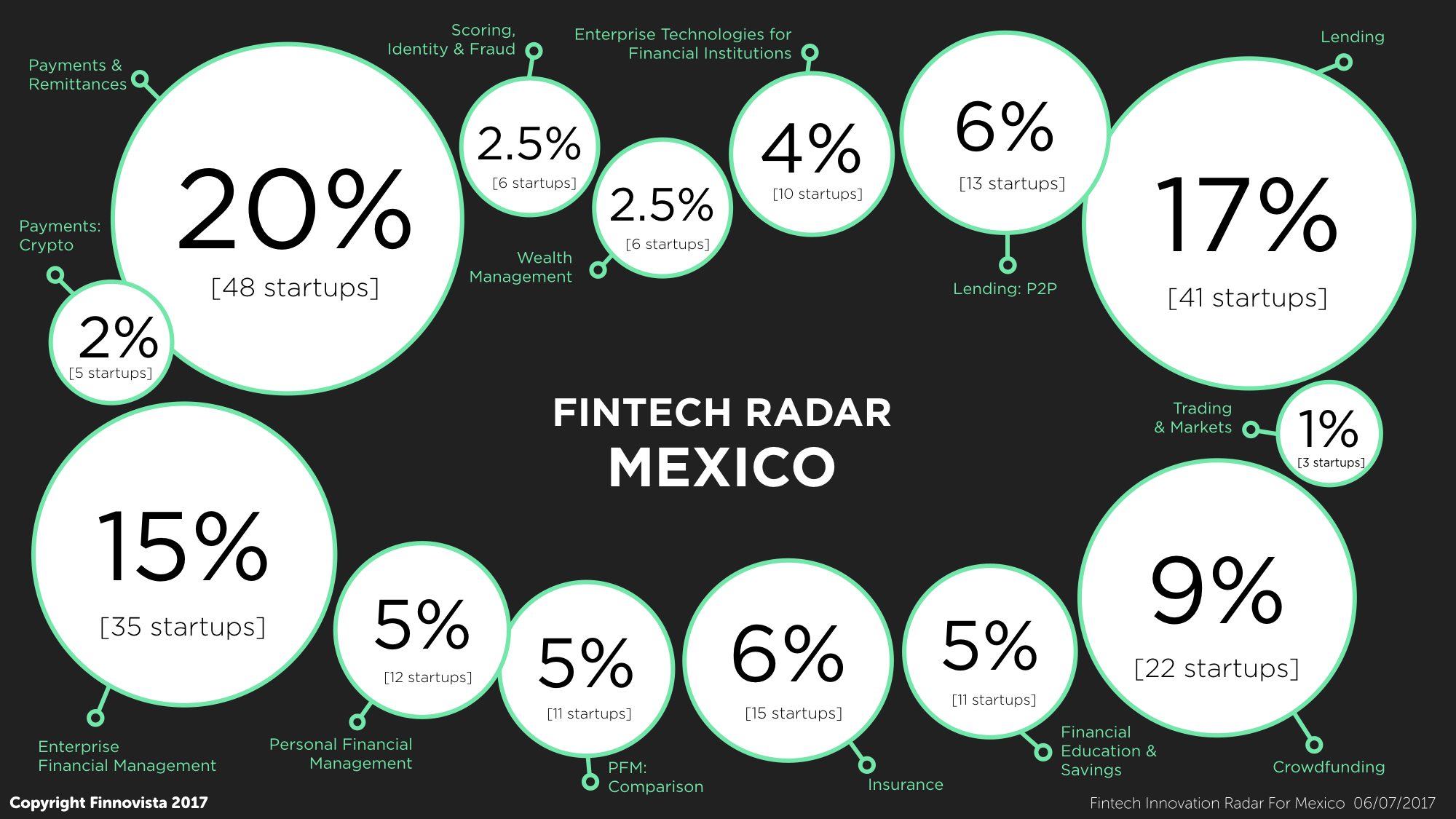

In this updated version of the Fintech Radar Mexico (July 6th, 2017) 238 mexican Fintech startups have been identified across 11 different segments, which represents a growth in the number of Fintech startups of 50% since the last edition published in August 2016, where 158 startups were identified. This means 80 new Fintech startups have been created in the last 10 months in the country. This figure positions Mexico as the largest Fintech ecosystem in Latin America, ahead of Brazil with 230 startups, according to the most recent report published by IDB and Finnovista in the second quarter of 2017.

A high Internet and smart mobile devices penetration, a strong ecosystem of entrepreneurship and e-commerce, a low banking penetration and an undeveloped consumer lending offer, are only a few of the particular features of the Mexican market that make the country one of the most fertile areas for the development of the Fintech industry. Moreover, Mexico’s economic growth in the last year was almost exclusively led by private consumption supported by low inflation, remittances and credit expansion, which emphasizes the role played by Fintech startups in the growth of the Mexican economy, as they offer more efficient and less costly alternatives compared to traditional credit and remittances services.

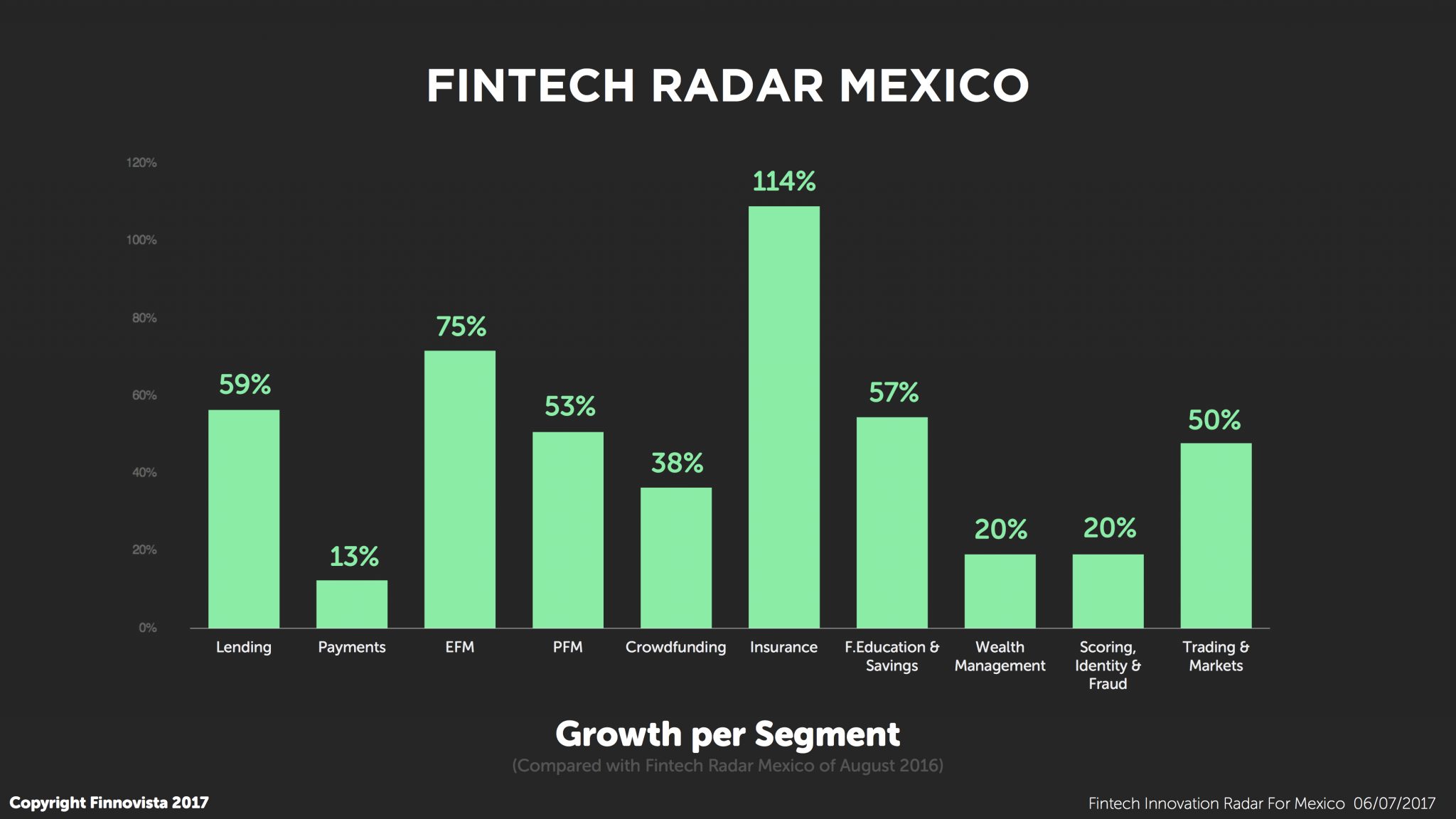

In comparison with the previous version of our Fintech Radar Mexico, this new analysis highlights relevant changes regarding the distribution and growth of the ecosystem players across the different Fintech segments, underlining the strong growth of the following segments: Insurance, Lending, Enterprise and Personal Finance, and Financial Education & Savings.

Currently, the six major Fintech segments in Mexico are:

- Lending, accounting for 23% of the identified startups

- Payments and Remittances, with 22% of the startups

- Enterprise Financial Management, covering 15% of the identified startups

- Personal Financial Management, with 10% of the startups

- Crowdfunding, accounting for 9% of the startups in the country; and

- Insurance, with 6% of the startups.

The remaining five Fintech segments are all under 5% of the identified startups in the analysis.

It is worth stressing that the Lending segment has increased 60%, occupying the first place in number of Fintech startups in the country, relegating the Payments and Remittances segment to the second place, after an exiguous growth of only 13%, which could indicate a saturation of the Fintech innovation in the payments segment in the country.

Another aspect to be noted in this new version, is the growth of the Enterprise Financial Management segment, which has consolidated its third position with a growth of 75% since the previous version of the Fintech Radar Mexico, accounting for 35 of the 238 identified startups. Other segments that also registered important growths were the Personal Financial Management segment and the Financial Education & Savings one, which grew 53% and 57% respectively since the last version of the Radar.

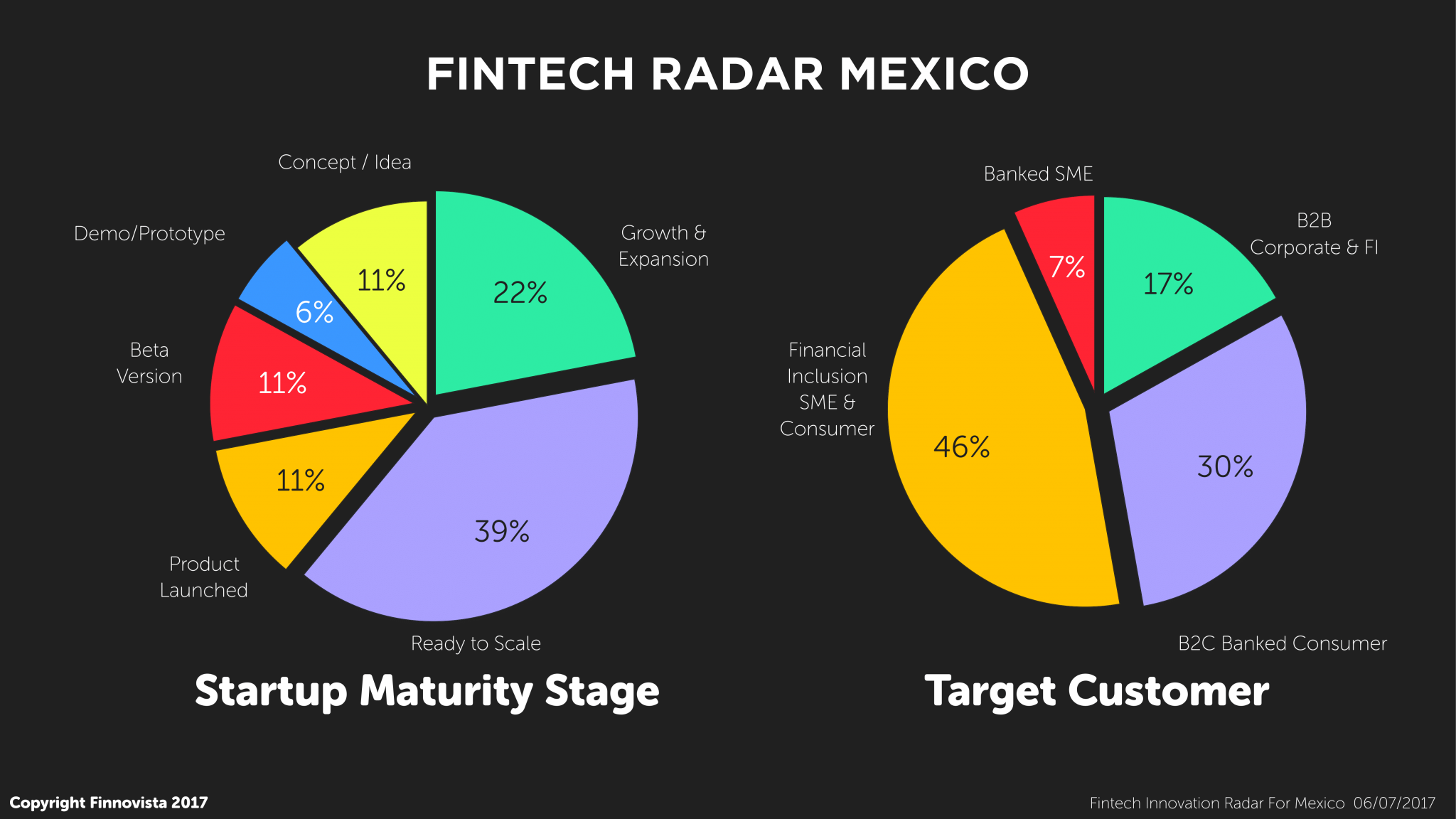

Regarding the maturity stage of Mexican Fintech startups, most of them say they are ready to scale (39%), while 22% position themselves in the Growth & Expansion stage. 39% of Mexican startups remain in initial stages.

When comparing the Fintech markets in Brazil (second biggest Fintech ecosystem of the region) and Mexico, it is worth noting that, while in Brazil 34% of the Fintech startups target their offer to enterprises and financial institutions (B2B transactions), in Mexico only 17% of startups focus towards this market. Regarding the offer towards banked consumers (B2C transactions), this offer applies to 30% of Mexican startups, similar to the 31% Brazilian startups.

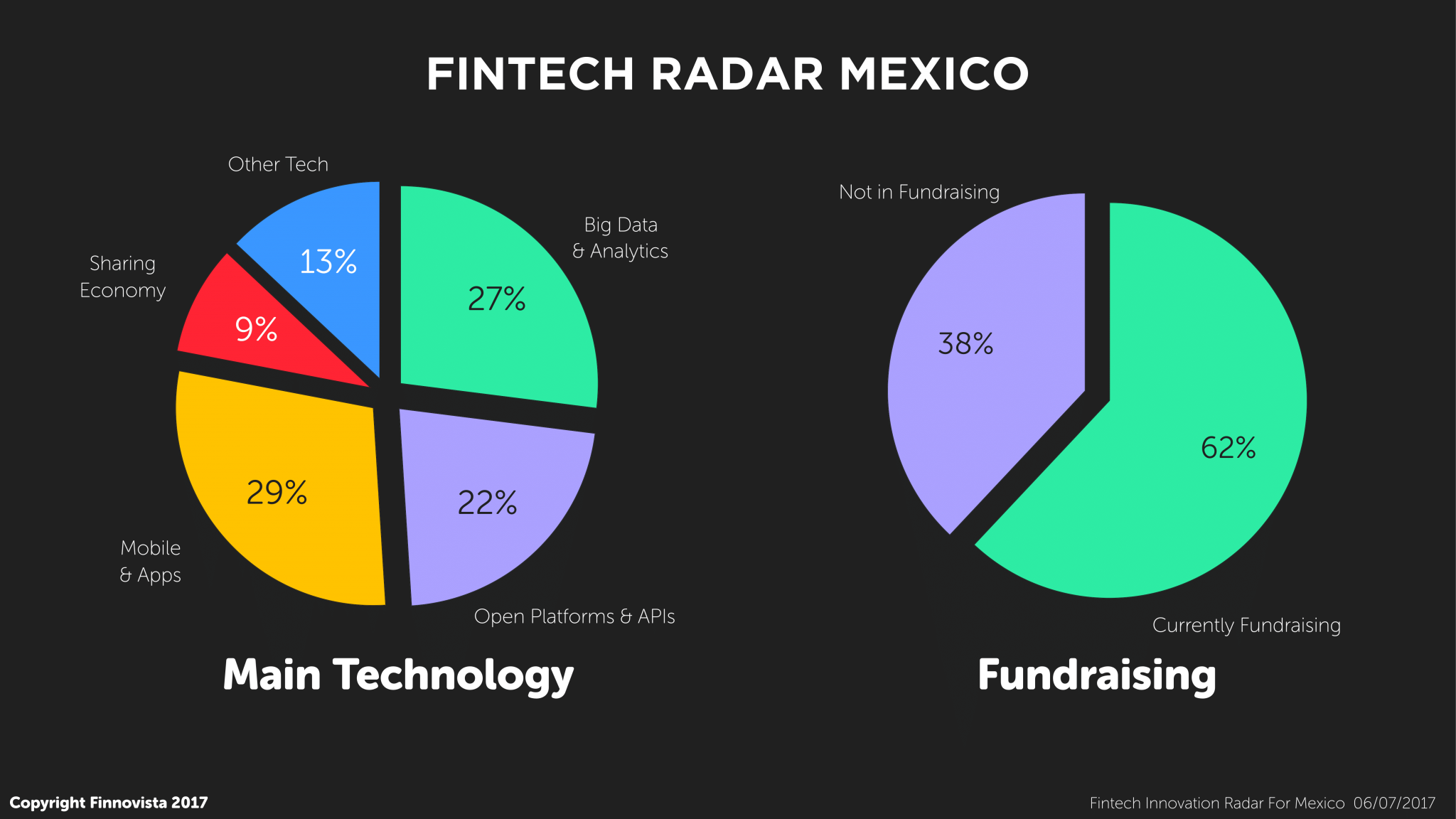

When asked about the main technology used to build their products and services, Mexican startups highlighted 4 technologies: Mobile and Apps (29% of startups use them), Big Data & Analytics (27%), API’s and Open Platforms (22%) and Sharing Economy (9%).

In terms of funding or fundraising, 63% of Mexican Fintech startups said they have received external funding in the past and, out of the 87 startups that accessed to respond about their financing plans, 62% stated that they are currently seeking out investment. These figures highlight the importance of fundraising and Venture Capital investment in the development of the Fintech ecosystem in Mexico.

Currently, the activities undergone by a large proportion of Mexican Fintech startups lie under areas that are not strictly regulated by prevailing applicable regulations in the country. This indicates that a specific regulation would have the potential to reduce operational risks, improve the transparency of technological platforms, establish high security standards to protect consumers and investors and build confidence around financial technology business models.

As all disruptive innovations, Fintech startups are breaking the status quo of the traditional financial industry. Consequently, this field is crucial for regulators of the Mexican financial system, which are drafting and supervising the draft legislation known as “Fintech Law”, to which companies of financial technology will have to align in order to operate in the Mexican market.

With a specific regulation on the brink and the arrival of leading players of the international Fintech scene, such as the world leader accelerator Startupbootcamp FinTech, which has recently launched its first program in Latin America based in Mexico, we conclude this analysis by making clear that Mexico is set to become a leading Hub for Fintech entrepreneurship in the region thanks to a number of social and economic factors that drive growth within the Fintech industry in the Mexican market.

From Finnovista, we would like to thank the following collaborators for participating in this Fintech Radar Mexico: Anette Urbina, Matthieu Albrieux, Amanda Jacobson, Pablo Prieto, and Francisco Junco. Thank you all for your support.

Do you know about any Fintech startup in Mexico that has not been included in our Fintech Radar?